What's the Real ROI? Motorized Screens, Aluminum Shutters & the True Cost of Doing Nothing

Every homeowner who considers hurricane protection or motorized screens for their Northeast Florida home eventually arrives at the same question: is it worth it?

The question is reasonable. The investment is meaningful. And the answer — when you calculate it honestly, with every relevant number on the table — is not close.

This post puts every number on the table. The insurance savings you are legally entitled to under Florida law. The storm repair costs you avoid. The furniture and UV damage you prevent. The energy costs you reduce. The resale value you add. And the cost most homeowners never calculate at all — the cost of doing nothing.

We are not going to give you a sales pitch disguised as math. We are going to give you the math. Then you can make the decision with real numbers, not guesses.

The Insurance Savings: What Florida Law Requires

This is the largest, most immediate, and most certain financial return on hurricane protection in Northeast Florida. It is not optional for insurers. It is state law.

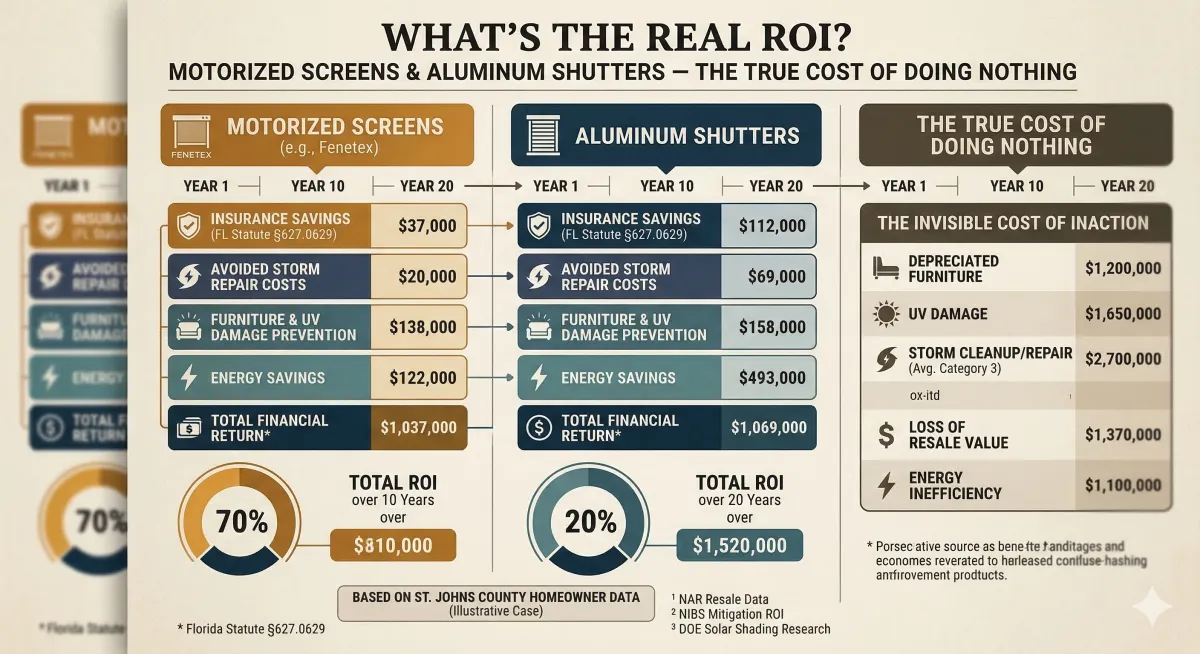

Florida Statute §627.0629 requires every insurance carrier writing homeowner's policies in the state to offer premium discounts for verified wind mitigation features. Hurricane shutters and hurricane-rated motorized screens are among the most impactful qualifying features.

Here is how the savings work in practice for homeowners in St. Augustine, Nocatee, Ponte Vedra Beach, and across St. Johns County:

Step 1: You install AHT aluminum hurricane shutters on windows and doors, and/or Fenetex hurricane-rated motorized screens on lanais and large openings.

Step 2: You schedule a wind mitigation inspection — a standardized assessment conducted by a licensed inspector who documents every hurricane protection feature on your home.

Step 3: The completed inspection form is submitted to your insurance carrier.

Step 4: Your carrier recalculates your premium, applying the wind mitigation credits mandated by §627.0629.

The typical savings range: 10 to 30 percent reduction on the wind and hurricane portion of your annual premium. In St. Johns County — where median home values exceed $400,000 and insurance premiums reflect the coastal and near-coastal exposure of the region — the wind and hurricane portion of a typical policy can represent $2,000 to $6,000 per year or more. A 10 to 30 percent credit on that amount translates to $200 to $1,800 in annual savings.

Over 10 years: $2,000 to $18,000 in cumulative insurance savings.

Over 20 years: $4,000 to $36,000 in cumulative insurance savings.

Those numbers are not projections. They are the mathematical output of a state-mandated discount applied to your actual premium. The only variable is the percentage your specific carrier applies — and that percentage is determined by the wind mitigation inspection results, not by negotiation.

Titan Outdoor Solutions provides all product documentation, Florida Product Approval numbers, and permit records your inspector needs to verify the installation. We have supported hundreds of wind mitigation inspections across Jacksonville, Palm Coast, and the surrounding service territory.

The homeowners who view hurricane shutters and screens as an expense are the ones who never ran the insurance math. The homeowners who view them as an investment are the ones who did.

The Storm Repair Costs You Never Pay

The second largest financial return is the one you measure in costs that never arrive.

As we documented in Week 8, traditional screen enclosures carry a recurring storm repair cycle that most homeowners do not anticipate when they purchase the enclosure. The mesh catches wind. The frame buckles. Contractors recommend cutting the screens before major storms and rescreening after.

The rescreening cost: $2,000 to $8,000 per event, depending on the size of the enclosure and the extent of frame damage.

Over a 20-year ownership period in Northeast Florida — a region that has experienced damaging storms from Hurricane Matthew (2016), Hurricane Irma (2017), Hurricane Dorian (2019), and Hurricane Milton (2024) — a homeowner with a standard screen enclosure can reasonably expect two to four significant rescreening events.

The cumulative storm repair cost for a screen enclosure over 20 years: $4,000 to $32,000.

The cumulative storm repair cost for Fenetex motorized screens over the same period: $0.

Motorized screens either retract before a storm (insect and solar mesh configurations) or deploy hurricane-rated OmegaTex fabric that absorbs wind and debris. In either scenario, the screen emerges from the storm intact. No rescreening. No frame repair. No post-storm contractor queue. No weeks of waiting with an exposed outdoor space.

The total storm repair savings over 20 years: $4,000 to $32,000 — a direct offset against the upfront investment in motorized screens.

The UV Damage You Prevent

The third financial return accumulates quietly — in the cushions that do not fade, the furniture that does not crack, the travertine sealant that does not degrade, and the interior furnishings near the glass that do not bleach.

We documented the full UV damage cost analysis in Week 6. Here is the summary for the ROI calculation:

Fenetex solar mesh blocks up to 91 percent of UV rays. It does not eliminate all degradation — some wear is inherent in any outdoor environment — but it slows the rate of damage dramatically. The furniture, cushions, and finishes that last three to four years in direct Florida sun last seven to ten years behind a solar screen.

The savings are real. The only question is where they fall within the range — and that depends on the quality and quantity of your outdoor furnishings, the sun exposure of your specific patio, and the fabric openness factor selected.

The Energy Savings Through the Glass

The fourth financial return comes from inside the house — specifically from the air conditioning system that runs less aggressively when the sliding glass doors behind your lanai are shaded by exterior solar screens.

As documented in Week 6, research from the U.S. Department of Energy indicates that exterior solar shading on south-facing and west-facing glass openings can reduce cooling energy through those openings by 25 to 40 percent.

In Northeast Florida, where air conditioning represents the largest single component of residential electricity costs from May through October, that reduction translates to measurable monthly savings. The specific amount depends on the size and orientation of the glass, the local electricity rate, and the HVAC system efficiency.

Conservative estimate over 20 years: $2,000 to $8,000 in cumulative energy savings — achieved simply by deploying solar screens on the exterior of the home's most sun-exposed glass during peak cooling months.

The Resale Value Contribution

The fifth financial return is realized when you sell the home — or when an appraiser evaluates the property for refinancing or equity purposes.

As we covered in Week 9, the National Association of Realtors (NAR) consistently reports that outdoor living upgrades return 80 to 100 percent of their investment at resale. In premium Northeast Florida markets — Nocatee, Ponte Vedra Beach, and the coastal St. Johns County communities — the return can exceed 100 percent for homes with completed, screened outdoor living rooms.

A home with a finished outdoor space — StruXure pergola, Fenetex motorized screens, outdoor kitchen, travertine patio — presents as a fundamentally different property than the same floor plan with a bare covered patio. Buyers perceive additional livable space. Agents highlight the year-round outdoor room as a differentiating feature. Listing photos show a finished, protected, usable space that competes against every other home in the neighborhood.

The resale contribution of motorized screens specifically is difficult to isolate from the broader outdoor living investment, but NAR's 80–100 percent return data on outdoor upgrades provides the framework. If your total outdoor living investment — including screens — is $80,000, the expected resale contribution is $64,000 to $80,000 or more.

The Cost of Doing Nothing: The Number Nobody Calculates

Here is the return most homeowners never quantify, because the costs are invisible until you add them up.

The cost of doing nothing for 10 years on a typical Northeast Florida home:

Read that range again. The low end — $22,000 — assumes minimal storm events, modest furniture, and average insurance premiums. The high end — $83,000 — reflects the reality of a coastal or near-coastal Ponte Vedra Beach or Palm Coast home with premium outdoor furnishings, elevated insurance costs, and multiple storm events over a decade.

These are not hypothetical costs. They are the actual, documented, recurring expenses that Northeast Florida homeowners absorb when their outdoor living space has no hurricane protection, no UV management, no insect barrier, and no storm-resilient enclosure system.

The investment in motorized screens and aluminum shutters does not merely pay for itself. In most scenarios for homes in St. Augustine, Nocatee, and across St. Johns County, it costs less than doing nothing.

The most expensive decision is the one that feels free. Doing nothing costs nothing today. It costs $22,000 to $83,000 over the next decade. The homeowners who understand that math are the ones who act in June — not the ones who act after the next storm.

The National Standard: $6 Returned for Every $1 Invested in Hazard Mitigation

For homeowners who want third-party validation beyond the specific numbers above, the National Institute of Building Sciences (NIBS) has conducted the most comprehensive study on hazard mitigation return on investment in the United States.

Their finding: for every $1 invested in hazard mitigation — including hurricane shutters, impact-resistant barriers, and wind protection systems — an average of $6 is returned in avoided disaster costs, reduced insurance claims, avoided displacement expenses, and preserved property value.

That 6:1 return ratio is not specific to motorized screens or aluminum shutters. It reflects the broader category of building protection investments in hurricane-prone regions. But it validates the specific ROI framework presented in this post: the combination of insurance savings, avoided repairs, preserved assets, and maintained property value consistently exceeds the upfront investment by a significant multiple.

The NIBS study is cited by FEMA, the Insurance Institute for Business & Home Safety, and the Florida Division of Emergency Management. It is the authoritative reference for the financial case that hazard mitigation is an investment, not an expense.

The Complete ROI Picture: Three Scenarios Compared

Here is the full financial comparison across three protection scenarios for a typical home in Nocatee or Ponte Vedra Beach over a 20-year ownership period.

Scenario C — the Titan combination of AHT aluminum shutters and Fenetex motorized screens — carries the highest upfront investment and the lowest total cost of ownership. It is also the only scenario that provides hurricane protection for outdoor living areas, blocks no-see-ums, delivers 91% UV reduction, and contributes meaningfully to resale value.

The Break-Even Timeline

For homeowners making the investment decision, the most actionable number is the break-even point — the year when cumulative savings and avoided costs equal the upfront investment.

The break-even timeline depends on the specific installation scope, insurance premium structure, storm frequency, and outdoor living investment size. But across typical Titan installations in St. Johns and Flagler counties, the break-even window falls within the following ranges:

Insurance savings alone: 7 to 15 years to break even — faster for homes with higher premiums and stronger wind mitigation credits.

Insurance savings + avoided storm repairs: 5 to 10 years — each rescreening event you avoid accelerates the timeline by $2,000 to $8,000.

Insurance + storm repairs + UV savings + energy savings: 4 to 8 years — the full ROI stack brings break-even into the first third of the system's 20+ year lifespan.

After break-even, every subsequent year is net positive return. The savings continue. The system continues to perform. The investment has paid for itself and is now generating ongoing financial benefit.

Financing: Making the Investment Work on Your Timeline

Titan understands that the upfront investment in a complete hurricane protection and outdoor living system is significant. That is why we offer financing options designed to make the investment work on your financial timeline.

Financing allows you to begin receiving the insurance savings, storm protection, UV prevention, and lifestyle benefits immediately — while spreading the investment cost over a period that aligns with the break-even timeline. In many cases, the monthly financing payment is partially or fully offset by the monthly insurance savings from the wind mitigation credit.

The result: you are protected from day one, enjoying your outdoor space from day one, and the investment is self-funding through the savings it generates.

Titan provides financing details during the proposal stage of every project. We present the investment alongside the projected insurance savings and break-even timeline so you can make the decision with complete financial transparency.

Frequently Asked Questions

Request Your Free ROI Estimate

Serving St. Augustine · Nocatee · Ponte Vedra Beach · Palm Coast · Jacksonville · Northeast Florida

Request a free ROI estimate with your quote — we will show you the projected insurance savings, resale impact, and break-even timeline for your specific home. The numbers tell the story. Let them.

Call or text: (904) 484-7580 | TitanOutdoorSolution.com